Some of them thought they were enrolling in a free government program to make their homes more energy-efficient. Others were promised the energy savings from their renovations would quickly offset the cost, only to end up with solar panels that didn’t work or were too few in number to make much of a difference. Some were signed up for projects that should never have been eligible for the financing to begin with, such as converting their garages to rental units. One answered a robocall about eliminating their electricity bill and wound up with an inoperable solar array and more than $20,000 of debt.

All of these homeowners were sold on a form of financing called property assessed clean energy, or PACE, which leverages the taxing authority of local governments to cover the high upfront cost of a climate-friendly home renovation.

PACE isn’t a mortgage, nor is it a conventional loan; rather, homeowners pay back their balance—plus interest—via a surcharge on their annual property taxes. Consumer attorneys and legal aid groups in large U.S. counties where homeowners have used PACE—including Broward, Miami-Dade, and Hillsborough counties in Florida and Los Angeles, Orange, and San Diego counties in California—say PACE has emerged as a serious problem for low-income homeowners. Those who can’t afford the steep interest rates on the financing may default on their property taxes or slip into mortgage foreclosure; attorneys have seen senior citizens take out new mortgages or sell their homes at a loss to get out from under the debt.

Allen Bowen of Los Angeles: an Army veteran and retired postal worker, Bowen used PACE in 2017 to install solar panels and energy-efficient windows on his 1,500-square-foot home near Los Angeles International Airport. A door-to-door contractor for Renovate America told Bowen that PACE was a government-backed program, he says, and rushed to start the job ¬before Bowen learned the cost: $10,331 added onto his annual property-tax payments. That’s more than a third of what he receives from his pension and Social Security. The solar panels didn’t work.Image: Philip Cheung for Bloomberg Green

More than 20 states offer PACE financing for commercial properties, but only three—Florida, California, and Missouri—make it available for residential dwellings. Still, homeowners far outstrip business owners as PACE users. At least 280,000 homeowners over the past dozen-or-so years have used the money to fund the installation of solar panels, energy-efficient windows, and other improvements, according to industry data. Most local programs outsource financing to private administrators, which in turn typically market and sell it via networks of home-improvement contractors. They repackage the debt itself into green bonds with attractive returns.

At least three more states are in the process of developing residential PACE programs, and with Joe Biden in the White House, the model could expand still further. On the campaign trail, he pledged to upgrade a total of 6 million aging buildings in the residential and commercial sectors, which together account for almost 40% of U.S. energy consumption. PACE is a readily available tool, especially for an administration eager to enlist private capital in the climate fight.

Solar panels on the roof of Bowen’s home.Image: Philip Cheung for Bloomberg Green

But consumer advocates say that, in practice, what’s on offer to homeowners can amount to a predatory loan with a green veneer. PACE financing is sold primarily by door-to-door contractors acting as de facto mortgage brokers, some of whom have allegedly targeted the elderly, non-English-speakers, and other vulnerable consumers.

Alysson Snow, a senior attorney at the Legal Aid Society of San Diego, says she first encountered the program in 2016 through an elderly client whose annual property taxes jumped from about $300 to more than $17,000 due to a series of clean-energy assessments. PACE is “basically a price-gouging, equity-stripping program that preys particularly on elderly folks who have the most equity in their houses,” she says. She’s currently representing more than a dozen different San Diego-area homeowners in litigation against major financing providers.

No government agency tracks how frequently the financing puts borrowers in jeopardy of losing their homes. The program’s proponents say that—when implemented as intended—PACE can be a vital tool in the fight against climate change. One 2018 study from researchers at the Lawrence Berkeley National Laboratory found that PACE resulted in a 7% to 12% increase in installations of residential solar systems in California cities that adopted it.

An inverter, part of a photovoltaic system, installed on the side of Bowen’s house.

Image: Philip Cheung for Bloomberg Green

“PACE is the only energy-efficiency and resilience-financing program that has ever achieved meaningful scale in the United States,” says Colin Bishopp, executive director of industry trade group PACENation. “The overwhelming number of homeowners who choose PACE have a positive experience.”

Around 2010 the city of Minneapolis considered launching a residential PACE program. Prentiss Cox, a law professor at the University of Minnesota who prosecuted subprime lending as a former Minnesota assistant attorney general, worked with his students to evaluate the plan. “None of the advantages are really true when you examine the programs,” he says. “The basic concept here is flawed.” The plan’s proponents told him, “ ‘We can get solar energy to people who couldn’t otherwise qualify for a loan,’ ” Cox recalls. “But it’s evolved into a very aggressive subprime marketing scheme.”

The plan in Minneapolis was never enacted.

Berkeley, Calif., launched the country’s first PACE program in 2008, two years after the city’s voters approved a ballot initiative calling for a local climate-action plan. Called a “world-changing idea” by Scientific American, PACE adapts the “special assessment district” model, whereby local governments issue bonds to raise capital for location-specific improvements such as parks and sidewalks, then repay them through a property tax levy. Berkeley’s program raised $1.5 million to fund residential rooftop solar installation. The program garnered national attention, and applications for the pilot filled up in 15 minutes. Localities such as Sonoma County, Calif., and Boulder County, Colo., quickly followed suit.

Biden, then the vice president, took notice and seized on PACE as a way to create green jobs while helping homeowners save money on their energy bills. In 2010 the U.S. Department of Energy announced $150 million in stimulus funds to help communities cover the operational costs of launching their own programs, part of a “recovery through retrofit” initiative meant to jump-start the construction industry in the wake of the housing market crash. PACE must be authorized by state legislatures; by 2011, more than 40% of them had given it the go-ahead.

Bowen’s home in South Los Angeles. Bowen kept up with the first three years of payments by borrowing money from family members. He’s now a lead plaintiff in a class action against Los Angeles County and Renovate America filed in 2018. Last year the county recommended cancellation of his lien, but he’s unable to recover more than $30,000 he already paid. Renovate America didn’t respond to requests for comment.Image: Philip Cheung for Bloomberg Green

The idea was a win-win for policymakers eager to claim environmental victories and investors desperate to find secure bets in a still-shaky market. But from the outset, the programs’ benefits for homeowners were less clear-cut.

By the time Berkeley published an initial evaluation of its pilot program in 2010, enthusiasm there had faded. Just 13 of the 40 homeowners initially accepted opted to move ahead with PACE financing. Many balked when they learned the terms on offer—an almost 8% interest rate over 20 years, a result of the PACE model’s reliance on private-placement bonds that typically require higher interest rates to entice investors. “The city acts as if they are doing the resident a big favor when there is no favor at all. Interest rate much too high,” wrote one homeowner who withdrew from the program, according to a city report. While some companies advertise interest rates as low as 4%, in 2019 40% of new assessments in California had rates from 8% to 12%, according to the state’s Department of Financial Protection and Innovation. That’s more than double the rate of a conventional mortgage and almost double that of most types of home-equity loan.

Blanca Garduno and Socorro Tamayo of Baldwin Park, Calif. Tamayo (right) was shocked in 2019 when her annual property tax payment jumped by more than $4,000. The previous year, Tamayo had solar panels installed on her roof, and she thought she’d enrolled in a program through her electric utility that would reduce her annual energy bill. She isn’t certain the solar panels are working, and her energy bill remains the same.

Image: Philip Cheung for Bloomberg Green

Another key selling point for investors in PACE-backed bonds—the security of repayment—also entails downsides for homeowners. Most programs designate PACE assessments as a “first-priority” lien, which gets paid back ahead of traditional mortgages. That raises the ire of mortgage lenders, who object to PACE investors cutting ahead of other creditors. As a result, homeowners with clean-energy assessments may find themselves unable to refinance their mortgage or sell their house unless they first pay off the assessment in its entirety.

In 2010 the Federal Housing Finance Agency announced that Fannie Mae and Freddie Mac, newly under government conservatorship, would no longer back new mortgages or refinance existing ones for properties with PACE liens, citing “significant risk to [mortgage] lenders.” That early setback blunted the program’s momentum and drew some unusual battle lines. PACE proponents—including several national green groups—depicted the program as the victim of mortgage-industry greed and pointed to its yet-unfulfilled environmental potential. Both the Sierra Club and the Natural Resources Defense Council sued, unsuccessfully, to overturn the FHFA rule.

“We can’t afford to waste our best ideas for saving energy,” wrote Michael Brune, executive director of the Sierra Club, in a 2012 Huffington Post op-ed encouraging readers to submit comments opposing the FHFA’s “misguided” policy. The Sierra Club declined to comment on its current position. Jay Orfield, NRDC’s director of buildings and energy for the Bloomberg American Cities Climate Challenge, says the bulk of his team’s current work on PACE focuses on commercial programs as opposed to residential ones, which are “more fraught.” Michael R. Bloomberg, the founder and majority shareholder of Bloomberg LP, the parent company of Bloomberg News, has promoted PACE through the American Cities Climate Challenge.

Tamayo’s home. Tamayo speaks only Spanish and asked her daughter, Garduno, to help her investigate. Garduno found paper forms at home showing her mother’s signature, authorizing the contractor to create an email address for her with the password Edison123, a reference to her electric utility. The password no longer worked, but Garduno eventually discovered that the address had been used to e-sign a PACE financing agreement with Renovate America, obligating her mother to repay more than $40,000 over 10 years. Image: Philip Cheung for Bloomberg Green

Despite support from progressive and environmental groups, consumer advocates say they saw red flags from the start. “At least in terms of how it operates, from a homeowner’s perspective, PACE is essentially a mortgage product,” says John Rao, an attorney with the National Consumer Law Center. But because it isn’t, technically, the financing isn’t subject to consumer protections put in place by the 2010 Dodd-Frank Act, including a requirement that lenders assess a borrower’s ability to repay before issuing a loan and a ban on mandatory arbitration clauses. Some PACE contracts require arbitration when disputes arise, and most contain the type of blanket liability waivers prohibited by the Federal Trade Commission in standard home-improvement contracts financed by banks. “There’s no reason PACE should be treated any differently,” Rao says.

The program’s advocates acknowledge that contractor fraud has occurred but chalk it up to cases of a few bad apples. Yet at least eight U.S. counties have ended their residential PACE programs because of consumer concerns, and major providers have been sued repeatedly for fraud, breach of contract, and related claims.

Homeowners have filed more than 40 such lawsuits against one of the country’s largest PACE providers, Ygrene Energy Fund, at least 25 of which are still pending in state courts. Ygrene (“energy” spelled backward) says it has been “needlessly dragged” into lawsuits against the contractors it works with to market its financing and has attempted to have some of the cases dismissed as nuisance suits.

Another major provider, Renovate America Inc., was facing more than 50 lawsuits when it declared bankruptcy in December. One of those was a class action brought by homeowners in Los Angeles County, which ended its PACE program in May 2020, citing “increasing criticism and concern” over consumer protections. In a related suit, L.A. County homeowners are pursuing yet another PACE provider, Renew Financial Group LLC, seeking cancellation of all the assessments it issued before California implemented ability-to-repay regulations in 2018. In filings, plaintiffs call the financing agreements “textbook examples of predatory loans.” Neither Renovate America nor Renew Financial responded to requests for comment, but in court filings each questioned the basis for the suits.

Solar panels on the roof of Tamayo’s home. Tamayo maintains she never saw the electronic documents she purportedly signed. “I’ve never sent an email in my life,” she says in Spanish. Garduno has helped her mother file complaints with California’s Department of Financial Protection and Innovation and two Los Angeles County agencies, to no avail. A representative from one county agency told her over the phone that because Renovate America has declared bankruptcy, it’s unable to help her, Garduno says.

A spokesperson for the county’s Internal Services Department says the county doesn’t comment on specific cases. The Department of Financial Protection and Innovation says the state continues to address complaints related to Renovate America but provided no further details. Renovate America didn’t respond to requests for comment. Image: Philip Cheung for Bloomberg Green

While L.A. County will no longer allow new PACE assessments, about 20,000 homeowners remain on the hook for outstanding liens. “Almost all of our clients are on a fixed or limited income,” says Jennifer Sperling, an attorney with the L.A.-based nonprofit legal clinic Bet Tzedek representing homeowner plaintiffs. “They never had any ability to pay back loans the size they’d been given.” A spokesperson for the county recommended that homeowners raise any issues directly with PACE administrators. California’s Department of Financial Protection and Innovation also says it’s committed to helping homeowners resolve complaints.

The Alliance of Californians for Community Empowerment helps Los Angeles-area homeowners fight foreclosure. The group began to focus on PACE about three years ago after receiving a stream of calls from homeowners who didn’t understand why their property taxes had doubled or tripled, according to Joe Delgado, director of ACCE’s Los Angeles office.

There was a common thread to the stories: contractors going door to door in low-income neighborhoods promising energy savings. Most PACE companies attempt to prohibit homeowners from challenging their assessments—for any reason—by burying broad waiver provisions in the contracts they sign. The agreements also indemnify the local government and PACE administrators.

Many of the homeowners who contacted ACCE spoke only Spanish but, under pressure, had signed documents in English, Delgado says. Some signed electronically on tablet computers carried by contractors who then vanished, leaving the homeowners tens of thousands of dollars in debt but with no paper trail. “We had never even heard of PACE at the time,” he adds. “Before long we had 100 people in our meetings, all dealing with a variation of the same scam.”

By adapting its methods for battling banks—call-ins, protests at corporate offices, town halls with elected officials—the group has gotten about a dozen homeowners’ PACE assessments rescinded. Dozens more remain at imminent risk of losing their homes, Delgado says.

Sandra Diaz of Cape Coral, Fl.Image: Zack Wittman for Bloomberg Green

Short of plying these tactics or going to court, defrauded homeowners have no clear path to relief, according to Snow of the Legal Aid Society of San Diego. “We have cases where no work was performed—not a hammer lifted—and the PACE administrator still won’t cancel the lien without litigation,” she says.

Under the rules of most PACE programs, administrators are supposed to provide homeowners with financing agreements to review before contractors begin work, as well as certificates to sign attesting that the work has been completed. But a rapid and typically digitized financing process leaves the door open for contractors to falsify applications and forge signatures before cashing out quickly, trapping homeowners in a maze of documents and debt. The problem recalls the frenzied lending in the runup to the housing crash. Snow says many of her clients had these documents sent to fake email addresses and signed electronically, presumably by the contractor. One client had their agreement with Renovate America e-signed using a disposable email address generated through yopmail.com, copies obtained through litigation show.

PACE administrators “want to pin the blame on these door-to-door salespeople,” Snow says. “But that’s the business model that they adopted.”

An air-conditioning unit behind Diaz’s home. Diaz was signed up for PACE during a 2018 visit from a contracting company whose owner has since been arrested for allegedly running a fraud ring involving the program. Diaz had wanted her air-conditioning ducts cleaned but ended up with a whole new system and a tax assessment that will cost her as much as $35,700. She and her husband were already struggling financially. Diaz has multiple sclerosis and receives disability; he works at a paper-shredding company. Image: Zack Wittman for Bloomberg Green

After California’s ability-to-repay rules went into effect, the volume of new assessments plummeted. But business is booming in Florida. Companies offering PACE financing there aren’t required to verify a homeowner’s income or creditworthiness, only that they’ve stayed up to date on their property tax and mortgage payments for the past three years. Loose standards for what makes a home improvement energy-efficient mean that air conditioners, skylights, and solar-heating for swimming pools all qualify.

By 2018, Sandra Diaz had lived in her Cape Coral, Fla., home for almost a decade. One day in July, her husband, Jose, spotted a bright-yellow truck parked in their neighborhood with a polar bear decal on the side and an advertisement for air-conditioning services. Diaz suffers from multiple sclerosis and spends almost all of her time in bed at home, which must be kept below 70F to avoid aggravating her symptoms. “I basically live in a box,” Diaz says. “I need it to at least be a comfortable one.”

On this day, Diaz was recovering from a respiratory infection, so the couple decided to call the number on the side of the truck hoping that someone could come and clean their ducts and help avoid future health complications for Sandra. By the next day, a representative from the air conditioning company—Bruno Total Home—had locked Diaz into a contract for an entirely new duct system, funded by a PACE assessment on the house, financed by Ygrene. The total cost of the system plus the work was almost $15,000; with interest, she could wind up paying as much as $35,700.

Diaz is one of at least a dozen homeowners in the Cape Coral area who say they were tricked or coerced into PACE financing—or had their signatures and personal information stolen or forged—by Bruno Total Home. Owner Louis Bruno was arrested last summer and charged with 40 counts of felony fraud, filing false documents, and related crimes. He has pleaded not guilty. In a related civil action filed last year, the Florida attorney general alleges that in numerous instances, the owner and his company used deceptive tactics to sign up customers for PACE financing.

Diaz’s backyard. Because of the lien on her house, Diaz is unable to refinance her mortgage to pay for the additional care and accommodations she needs as her illness progresses. Ygrene Energy Fund, which provided the financing, says it’s working to address complaints from the contractor’s customers on a case-by-case basis, but that it’s not liable for its contractors’ actions.

Image: Zack Wittman for Bloomberg Green

Ygrene says Diaz received all of the disclosures necessary to understand the financing she agreed to. Yet an examination of the paper trail—including a series of calls between Diaz and Ygrene representatives recorded by the company—shows how Ygrene’s stated consumer protection policies can fail to protect the consumer.

The company’s program guidelines and agreements give homeowners three days to cancel the financing, a policy that’s intended to protect homeowners from pushy contractors. But when a Ygrene representative asked Diaz during a standard “welcome call” if she wanted to waive this right, Diaz responded that the contractor had already started work—just one day after she and her husband made their initial call to Bruno Total Home.

That should have been “an immediate flag that the contractor had violated the program requirements,” according to the National Consumer Law Center’s Rao, who reviewed the recording. Instead, the Ygrene rep noted that Diaz was waiving the right to cancel and completed the call. A “notice to proceed” was issued to the contracting company the same afternoon.

Ygrene says the representative explained all of the terms of the financing agreement to Diaz on the welcome call, and both Ygrene and an attorney for Bruno say it was Diaz’s decision to have the work start early. When Cape Coral police interviewed former Bruno Total Home employees during the investigation of Bruno, several said that while Ygrene guidelines told contractors to wait until the three-day period expired, Bruno directed his employees to start jobs immediately so customers wouldn’t be able to cancel.

While the Ygrene representative made a passing reference to a “PACE lien” during the welcome call, Diaz says she didn’t understand the financing would result in a lien on her home until months later, when she tried to refinance her mortgage. Now, “I feel more trapped than ever,” she says.

Eventually, another former Bruno employee submitted a written statement in court, as part of a civil suit Diaz brought against Bruno and his company, saying he’d falsely notarized a document that was purportedly signed by Diaz and verified using her driver’s license. Diaz is physically unable to drive, according to court documents, or even write her name due to her MS. Bruno denied Diaz’s allegations through his attorney in the case.

Ygrene says that it terminated Bruno Total Home from the PACE program before any criminal allegations were made and that it’s worked to assist property owners in resolving outstanding issues related to the contractor. It also says its contractor-compliance team vets all potential contractors and provides ongoing training and monitoring, but it maintains that it’s not liable for the actions of its contractors, including those who formerly worked for Bruno. Unless she’s able to squeeze an additional $1,700 a year out of her disability assistance to pay the increased taxes, Diaz could end up losing her home.

Mike Fasano, the tax collector for Florida’s Pasco County, has seen the consequences of lax regulations firsthand. As part of his duties, Fasano is obligated to collect annual PACE assessments and sell tax certificates for delinquent properties. After seeing problems mount in the county, he hired an in-house customer advocate and created his own two-page disclosure form to make sure would-be customers were fully informed of the risks. Homeowners have to print and sign the form before their PACE assistance can be finalized, according to Fasano’s contract with PACE administrators.

“Someone’s got to protect the consumer,” he says.

As climate change has intensified, so too has pressure to expand PACE for the benefit of homeowners forced to retrofit for protection against storms and wildfires. But where it may mitigate climate risks, PACE introduces financial ones. Where it’s used for residential homes, the model rests the financial burden of the climate transition on individuals who may be least able to shoulder it.

After years of largely unchecked expansion, advocates hope to see regulations catch up to PACE. The U.S. Consumer Financial Protection Bureau is working on a rule to establish ability-to-repay requirements and allow consumers to recover damages and get help defending against foreclosure. Combined with state protections and oversight, that could keep some of the biggest problems in check. “The key is having local government entities deeply involved, not just lending their name and taxing [authority] to the project,” Rao says.

Even then, a patchwork of local programs is no substitute for ambitious federal action. And of all the daunting investments needed for the U.S. to reach net-zero emissions—from overhauling the power grid to building out mass transit—boosting the energy-efficiency of American homes may be the easiest pitch politically. Done right, it’s a boon for homeowners and a bonanza for green jobs. And federal intervention to transform the housing market has some familiar precedents: from New Deal programs that rapidly expanded home ownership to a brief but successful stimulus for housing weatherization in the aftermath of the financial crisis.

Today, federal programs for retrofitting reach no more than 1% of existing U.S. buildings each year, according to Laurie Kerr, a former deputy director for New York City’s office of sustainability. While private capital can play a role, she advocates a dramatic expansion of direct federal investment in home energy efficiency, starting with low-income housing and public buildings. “At the pace that we’re going, it would take centuries” to upgrade the building stock, Kerr says. “We don’t have that kind of time.”

Climate activists have no shortage of ideas for how to get there sooner, from a national bank that would back climate innovation to green loans from the Fed to expanding federal backing for mortgages so they include qualifying home retrofits and electrification. But any of these policies would require substantial buy-in from both legislators and ordinary homeowners.

“When you have a product that’s going to leave people with a sour taste about alternative energy when you see how it plays out in people’s lives, that’s a negative for getting public support for the kind of policies you need,” says Cox, the Minnesota law professor. “We need programs that work, not abuse people,” he adds. “If we end up with entire communities who hear the words ‘solar energy’ and say, ‘Quick, shut the door,’ that’s not helping the cause.”

—With Zeke Faux.

Who Pays the Most for PACE?

According to ratings agency data, tax delinquency rates for properties with clean-energy assessments are lower than delinquencies overall.

But looking only at property-tax woes may miss the bigger picture. Many homeowners pay their property taxes through an escrow account linked to their mortgage, so if they get into financial trouble, it would be with their mortgage company, not the tax collector. Neither ratings agencies nor program administrators—nor any government agency—tracks post-PACE mortgage delinquencies.

Bloomberg Green and Type Investigations analyzed property records in Broward County, one of the two largest markets for PACE in Florida. The county makes property-deed data available publicly; it also provided a full list of clean-energy assessments on its tax rolls.

For 2019, the most recent year for which data was available, property-tax delinquencies for PACE properties were lower than the overall rate. There were more mortgage foreclosure cases than tax delinquencies, which is noteworthy given that homeowners must be current on their mortgage to be approved for PACE.

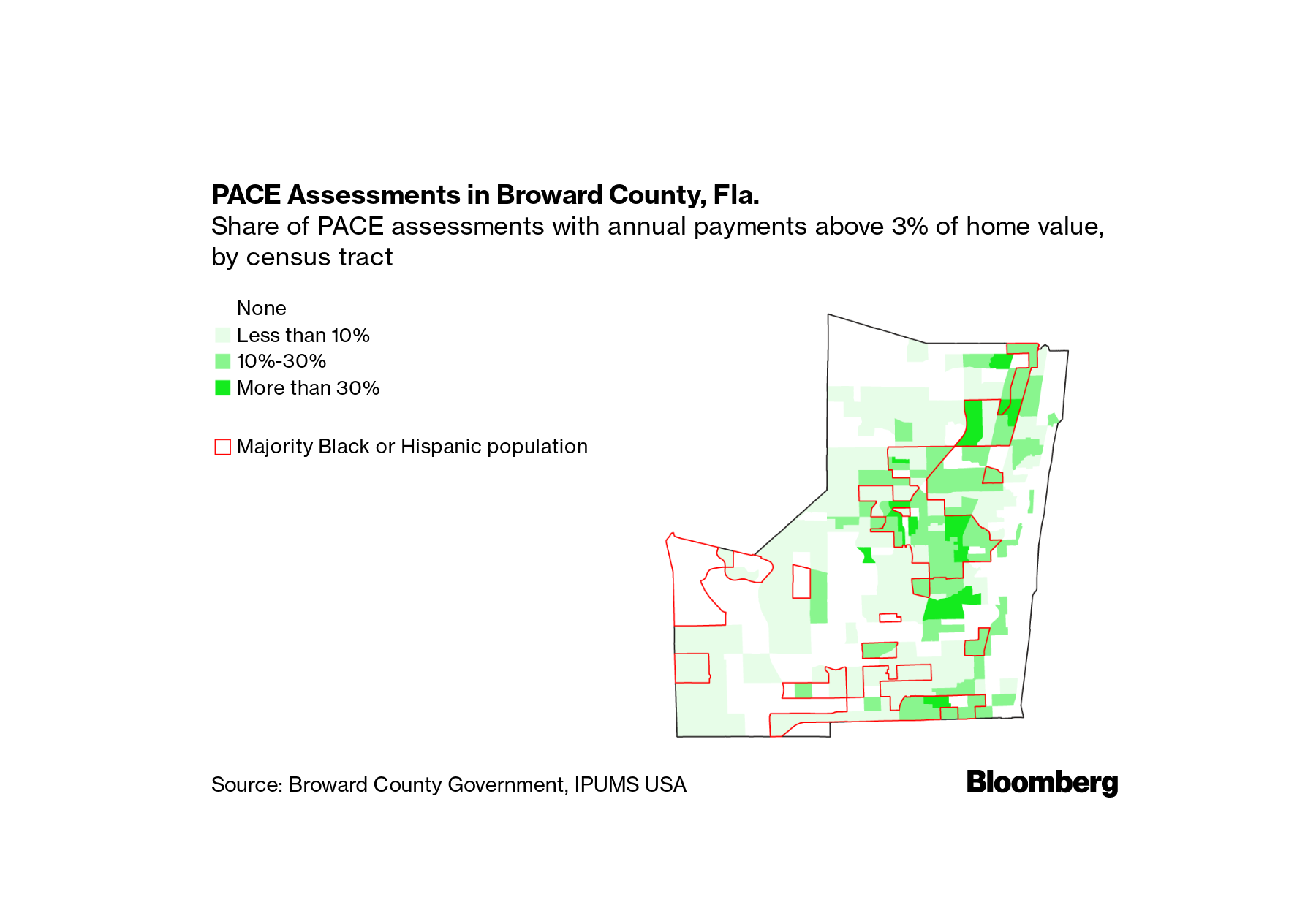

The story changes considerably, though, once time is factored in. The majority of Broward County homeowners with PACE assessments have only faced one or two annual payments, while those who’ve been paying for longer appear to have run into more problems. Those whose assessments first hit the tax rolls in 2016 faced foreclosure at more than double the rate of those whose first payment came due in 2019.

Florida law limits the size of a PACE assessment relative to a home’s value but doesn’t take interest payments into account. The map above breaks down census tracts in Broward based on the prevalence of assessments with annual payments—including interest—that exceed 3% of the home’s appraised value. Many of those with the highest debt burdens are in majority minority zones. —With Geoff Hing